BSEB Bihar Board 12th Business Economics Important Questions Long Answer Type Part 1 are the best resource for students which helps in revision.

Bihar Board 12th Business Economics Important Questions Long Answer Type Part 1

Question 1.

Explain the law of demand with the help of a diagram. Explain any five factors affecting the demand of a commodity.

Answer:

Law of demand: The law of demand stages that, other things being equal the demand for a good extends with a decrease in price and contracts with an increase in price. There is inverse relationship between quantity demanded of a commodity and its price, provided other factors influencing demand remain unchanged. The law of demand states that other things remaining constant quantity demanded of a commodity increases, with a fall in price and diminishes when price increases.

Factors affecting demand:

(i) Utility of the goods: Utility means wants satisfying power of a commodity. It is a subjective factor which varies from personal to person. Goods having greater or more utility will be in greater demand and vice-versa.

(ii) Income level: Income level directly affects demand. Higher the level of income, higher will be the demand and lower the level of income, lesser will be the demand.

(iii) Distribution of wealth: Distribution of wealth also affects demand. If the distribution of wealth in society is unequal, then luxuries goods will be demanded by affluent section of society. But as the distribution of wealth becomes equal, there will be increased demand of necessary and comfortable goods.

(iv) Price of the Goods: Price of the goods directly affects the demand for it. At a lower price, demand will become high and vice-versa.

(v) Expected future change in price: Govt, regulation natural calamities, possibility of war, etc. affects demand of goods.

Question 2.

Briefly explain the main functions of a commercial Bank.

Answer:

A commercial bank is a financial institution which accepts deposit from the public and advances loans to other. The main functions that commercial banks perform are:

(i) Accepting of deposits: Commercial banks receive money from the public and bussinessman in form of deposits. People can deposit their cash balances with a bank in either of the following accounts: (a) Current Deposit A/c (b) Fixed Deposit/Term Deposit A/c (c) Saving Deposits A/c and (d) Recurring Deposits A/c.

(ii) Advancing of loans: Commercial banks provide various type of loans to the borrowers in either of the following forms: (a) Cash credit (b) Term loans (c) Demand loans (d) Overdrafts (e) Discounting of Bills Exchange.

(iii) Investment of funds: The banks invest their surplus funds in three types of securities (a) goverment securities (b) other approved securities (c) other securities.

(iv) Agency functions: The banks pcrfomi the following agency functions for its customers for a commission (a) Transfer of funds through demand draft mail, transfer, telegraphic transfers etc. (b) Collection and payments of cheque, bills of exchange and dividend on behalf of the custefncrs. (c) Acting as executors and trustees of Wins.

(v) General Utility Services: Commercial banks provides following services of general utility to its customers: (a) Locker facility (b) Traveller’s cheques (c) Gift cheques (d) Undertaking securities (e) Purchase and sale of foreign exchange.

Question 3.

Distinguish between Micro Economics and Macro Economics.

Answer:

Distinction between Micro and Macro Economics: Micro and Macro Economics are two main branches of Economics. Micro Economics deals with individual economic problems whereas Macro Economics is the study of aggregates or of entire economic system. These two approaches differ from each other in the following manner:

Micro Economics:

1. It is concerned with an individual economic unit like a consumer, a firm, an industry or income of an individual.

2. It is based on the assumption of full employment.

3. Its central problem is price determination.

4. What is true at micro level may not be true for macro level.

5. It is based on the assumption of ‘other things being equal.’ This analysis is based on partial equilibrium.

6. Its objective is to study the theories related to optimum distribution of resources.

7. Its nature is comparatively easy.

8. It has main instruments of demand and supply.

Macro Economics:

1. It deals with aggregates of economy such as national income, aggregate expenditure, total employment, general price level, etc.

2. It is based on the assumption of under full employment of resources.

3. Its central problem is production and employment determination.

4. Group behaviour is applicable on entire economy.

5. This is based on general equilibrium analysis.

6. Its objectives is to study the theories related with full employment.

7. Its price is comparatively complex.

8. Its main instruments are aggregate demand, aggregate supply, aggregate saving and investment.

Question 4.

State the relation between total utility and marginal utility?

Answer:

The relation between total utility and marginal utility are as follows: Total Utility is defined as the total satisfaction a consumer obtain from a given amount of a particular commodity Total utility is the sum of the marginal utilities obtained from the consumption of different units of a commodity i.e.,

TU = MU1 + MU2 + ……….. MUn = ΣMU.

Marginal utility is an addition made total utility by consuming-an additional (extra) unit of a commodity. Symbolically, MU = ΔTU/ΔQ or MUn+n = TUn – TUn-1

Relationship between TU and MU: (i) so long as MU is positive, TU rises (ii) When MU becomes zero, TU is maximum and (iii) when MU is negative, TU falls.

Question 5.

Distinguish betwen fixed cost and variable cost.

Answer:

Fixed cost are the costs which do not change with the change in output. These costs remain even if the output is zero. Examples of total fixed costs are rent for factory building wages to the permanent staff, interest capital etc.

Variable costs are the costs which change with the change in the output. There are no variable costs at zero-output. Example of total variable costs are expenses on raw materials used in the production, wages of the capital laborers etc.

Question 6.

Discuss the Central Problem of an economy.

Answer:

According to prof Samuelson, every economy has three basic problems of resource allocation:

(a) What to produce and in what quantity?

(b) How to produce?

(c) For whom to produce?

(a) What to produce and how much to produce?

The very first central problem of economy is related to problem of choice. First and foremost problem of economy is- What to produce or which goods and services should be produced so that maximum wants and needs of people could be satisfied with limited resources. Every economy has to choose that which want should be satisfied and which should be sacrified, postponed or left? Regarding what to produce? Many production related options come before us for the solut ion of this problem.

When an economy decides what to produce; then next problem appears i.e. ‘How much to produce’? or we have to decide that what quantity of consumption goods and capital goods should be produced? For example, if an economy wants to increase production of consumer goods like clothes and tea through limited resources in a definite time-interval then it has to reduce production of capital goods like tractor and television. Infact, producer would like to produce that quantity of goods which maximises his profit.

On the basis of this choice, through available alternatives, a country has to decide that what quantity of limited factors should be used for producing which quantity.

(b) How to produce?

Second problem before the economy is ‘how to produce’? In fact, it is the problem related to the choice of technique. There are two types of techniques of production:

- Labour-intensive Technique: In this technique, more quantity of labour is used as compared to capital.

- Capital-intensive Technique: In this technique, more quantity of capital is used as compared to labour.

For example, clothes can be produced by both, handloom (i.e. capital-intensive technique).

How to produce?-for solution of this problem, we should adopt that technique which utilises lesser limited resources. If the production from both the techniques is the same then the technique using less quantity of limited resources will be called more efficient technique.

(c) For whom to produce?

After getting the solutions of the problems of what? how much? and how? the next problem arises-”For whom to produce”? or “How to distribute the production?”

There are two faces of the problem of distribution of production:

(a) First face is related to ‘Personal Distribution’. It means that how the produce should be distributed between different persons and families in the society. It is also related to the problem of unequal distribution of income.

(b) Second face of the problem of distribution is ‘Functional Distribution’. It is related to determine how the produce should be distributed among various factors of production as land, labour, capital and entrepreneur. It is not related to problem of inequality of income distribution.

Question 7.

Discuss the different types of Economics Systems.

Answer:

Economic Systems: Economic system is a structure of such institutions with which all economic activities are operated in the society. Every economy is based on an economic system which can be divided into three categories:

- Capitalist Economy or Market Economy,

- Socialist Economy or Planned Economy,

- Mixed Economy.

(1) Capitalist Economy or Market Economy: Market economy contains the following important features:

- Private Property: Capitalist economic system recognises ‘Law of Inheritance’ and right of individual private property. It also ensures to transfer the property of dead person to its heir.

- Economic Freedom: Capitalist economy grants various economic freedoms to the individual like freedom to work, freedom of choice, freedom of consumption and freedom of saving and investment.

- Laisscz Faire & Free Trade: Market economy works under Laissez Fairc i.e., there is no state intervention in economic activities of the society. Market economy is an open economy in which free trade policy is adopted.

- Competition: Competition is an essential feature of market economy. Equilibrium between market forces, i.e., demand and supply takes place due to competition appearing in the economy.

- Price Mechanism: In capitalist economy prices are determined by the automatic adjustment of price mechanism. Price in the market is determined at the point where demand and supply forces become equal.

(2) Socialist Economy or Planned Economy: The salient features of Controlled Socialist Economy are as follows:

- Social Ownership: In socialist economy social ownership is found on factors of production. These factors are used for the welfare of the society as a whole. Right to individual property has no place in socialist economy rather it is limited to only self-consumption goods.

- Absence of Economic Freedom: Individual economic freedom remains absent in socialist economy. What? How? and How much? problems arc solved by centralised planning institution according to the needs of the society.

- Passive Role of Price Mechanism: In socialist economy, prices are not determined by price mechanism, rather government takes the use of accounting prices which are determined by government itself on the basis of social interest.

- Absence of Competition: Socialist economy works on planning and direction, as a result of which competition remains absent in the economy.

(3) Mixed Economy: Mixed Economy contains the following economic features:

(i) Co-existence of private and Public Ownership: Private and public sectors co-exist in the mixed economy. Both private ownership and profit motive arc found in such economic system. Law of Inheritance finds a place in the economy but government imposes progressive taxation to attain economic equality.

(ii) Economic Freedom: Though enough state interference is found in Mixed Economy, people enjoy limited economic freedom of choice, production, investment and saving. Govt, adopts many controls so check the unlimited economic freedom of the individual.

(iii) Price System: Both price mechanism and profit motive determine the price system simultaneously in the Mixed Economy. Profit motive is managed by the government so that it may not hit the motive of social welfare.

(iv) Limited Competition: Mixed Economy contains limited competition due to the co-existence of both private and public sector. Competition appears in the economy but due to government regulation, economic development activities are not adversely affected.

Question 8.

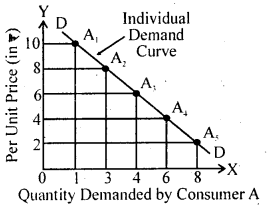

Explain ‘Individual Demand Curve’ and ‘Market Demand Curve’ with the help of figures.

Answer:

Individual Demand Curve: Individual demand curve shows various combinations of the quantity of goods demanded by an individual consumer at different prices. Individual demand schedule has been shown in fig. Quantity demanded by consumer A has been represented on X-axis and

per unit price on Y-axis. When price of goods is ₹ 10 per unit, he buys only one unit of it. When price decreases to ₹ 8 per unit, quantity demanded increases to 3 units. Demand curve DD slopes downward from left to right, which shows that when price decreases, demand increases and vice-versa. In this way, the individual demand curve is negatively sloped.

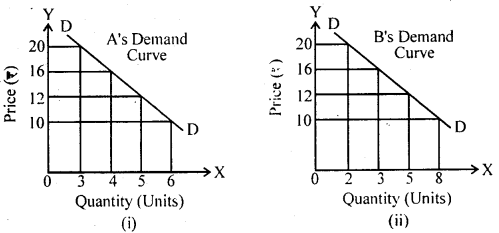

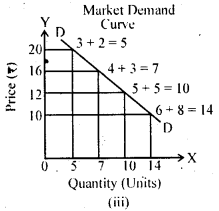

Market Demand Curve: By represeting market demand schedule on a graph, we can obtain ‘Market Demand Curve’. This curve represents demand of goods at different price for all the consumers in the market. Market demand curve is a horizontal summation of individual demand curves.

In fig., quantity of milk has been shown on X-axis and price of milk on Y-axis. In panel (i) and (ii), individual demand curve of consumer A and B has been represented.

In panel (iii), market demand curve has been represented. When price of milk is ₹ 10 per litre, then consumer A and B demand 6 and 8 litres of milk respectively. Hence, at price ₹ 10, market demand is 6 + 8 = 14 litre of milk. In this way, market demand curve is obtained by adding individual demand curves. It is horizontal summation of individual demand curves. Its slope is negative which shows the inverse relationship between price and quantity demanded.

Question 9.

What is Law of Demand? Why does the demand curve slope downwards? Are there exception to it?

Answer:

Law of Demand: Law of demand explains quantitative relation between price of goods and quantity demanded. Every consumer has a psychology to buy less amount or quantity of anything at high price and more quantity at low price. Ceteris paribus (other things being equal), there is inverse relationship between price of a goods and quantity demanded i.e. when price is high, demand is low and when price is low, demand is high.

In other words, there is an inverse relation between price of a goods and its demand. When price increases, demand decreases and vice-versa. Law of Demand is a ‘qualitative statement’ and not a ‘quantitative statement’. This law locates the direction of price and demand change and not the quantity of change.

P ∝ \(\frac{1}{\mathrm{Q}}\)

where, P = Price of Commodity

Q = Quantity Demanded

Assumption of the law of Demand: Law of demand is based on few assumptions. Those assumptions are:

- Consumer’s income should remain constant.

- Consumer’s taste, nature, etc. should remain constant.

- Price of related goods should remain constant.

- Consumer remains unknown with new substitutes.

- There is no possibility of price change in future.

Why Demand Curve slopes Downward?

Slope of demand curve is negative, i.e., it fails from left to right which means that less goods are bought or demanded at high prices and vice-versa. Negative slope of demand curve is due to following reasons:

(1) Law of Diminishing Marginal Utility: Law of demand is based on law of dimishing marginal utility. According to it, marginal utility of a goods diminishes as an individual consumes more units of a goods. In other words, as a consumer takes more units of a goods, the extra utility or satisfaction that he derived from an extra unit of the goods goes on falling. The law of diminishing marginal utility means that the total utility increases but at a decreasing rate.

Marshall has stated this law as:

“The additional benefit which a person derives from a given increase of his stock of a thing diminishes with every increase in the stock that he already has.”

At low price, more units of a goods is demanded and vice-versa.

(2) Increase in Purchasing Power or Income Effect: When price of a goods decreases, real income or purchasing power of consumer increases due to. which he can maintain his previous level of consumption with less expenditure. In this way, at lower prices, more goods could be purchased. On the contrary, when price of a goods increases, real income of consumer decreases due to which his consumption decreases. This is the law of demand.

Question 10.

What is Perfect Competition? What are its main characteristics?

Answer:

Perfect Competition: Perfect competition is that market situation in which a large number of buyers and sellers are found for homogeneous product. Single buyer or the seller are not capable of affecting the prevailing price and hence, in a perfectly competition market, a single market price prevails for the commodity.

Definitions:

- According to Ecftwitch, “Perfect competitve is a market in which there are many firms selling identical products with no firm large enough relative to the entire market to be able to influence market price.”

- According to Mrs. Joan Robinson. “Perfect competitive prevails when the demand for the output of each producer is perfectly elastic.”

Characteristics or Features of Perfect Competition:

(1) Large Number of Buyers and Sellers: Perfect competitive market has a large number of buyers and sellers and hence, any buyer or seller cannot influence the market price. In other words, individual buyer or seller cannot influence the demand and supply conditions of the market.

(2) Homogeneous Product: The units sold in the market by all sellers are homogeneous (or identical) in nature.

(3) Free Entry and Exit of Firms: In perfect competition, any new firm may join the industry or any old firm may quit the industry. Hence, there is no restriction on free entry or exit of firms into/from the industry.

(4) Perfect knowledge of the Market: In perfect competition, every buyer has the perfect knowledge of market conditions. None of the buyers will buy the commodity at higher price than the prevailing price in the market. Hence, only one price prevails in the market.

(5) Perfect Mobility of Factors: In perfect competition, the factors of production are perfectly mobile. Factors can easily be mobile from one industry to other industry (or from one firm to other firm) without any difficulty.

(6) No Transportation Cost: Transportation cost remains zero in perfect competition due to which one price prevails in the market.

Question 11.

What is meant by Monopoly? Mention the main features of Monopoly Competition.

Answer:

Monopoly is the addition to two words, i.e., ‘Mono’ + ‘Poly’, i.e. single seller in the market. Being the single seller in monopoly market, a firm has full control on the supply of the commodity. In pure monopoly even no close substitute of the product is available in the market.

In monopoly, no distinction arises between ‘firm’ and ‘industry’ i.e. firm is industry and industry is firm.

Definitions:

(1) According to McConnell, “Pure monopoly exists when a single firm is the sole producer of a product for which there are no close substitutes,”

(2) According to Braff, “Under pure monopoly there is a single seller in the market. The monopolists demand is market demand. The monopolist is a price-maker. Pure monopoly suggests a no substitute solution.”

(3) According to Leftwitch, “Pure monopoly is a market situation in which a-singlc firm sells a product for which a single firm sells a product for which there arc no good substitutes. The firm has the market for the product all to itself. There are no similar products whose price and sales will influence the monopolist’s price or sales.”

Features of Monopoly: The main features of monopoly are as follows:

(1) Single Seller and Large Number of Buyers: Monopoly market consists single seller of the product but the number of buyers stands very large.

No buyer can influence the price of the product due to his large number in the market.

(2) No Close Substitutes: Monopoly firm produces such commodity which has no close substitute and as a result the cross elasticity of demand becomes zero.

(3) Monopolist as a Price-maker: Being the single seller in the market, the monopolist firm is itself a price-maker. A monopolist firm can determine both price and quantity but not simultaneously (i.e., either price or quantity at a particular time).

(4) No Entry of New Firm: The entry of new firm into the industry is strictly prohibited. There is no competitor of monopoly firm in the market.

(5) Demand Curse Negatively Sloped : Monopolist demand curve is negatively sloped and marginal revenue (MR) is less than average revenue (AR). The slope of demand curve depends on elasticity of demand.

MR = AR\(\left(\frac{\mathrm{e}-1}{\mathrm{e}}\right)\)

or, AR = \(MR\left(\frac{\mathrm{e}}{\mathrm{e}-1}\right)\)

Question 12.

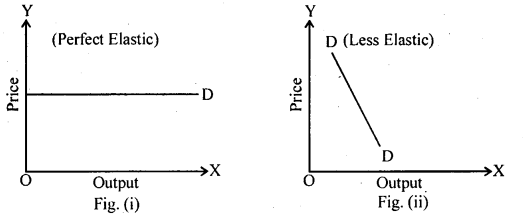

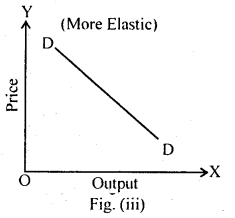

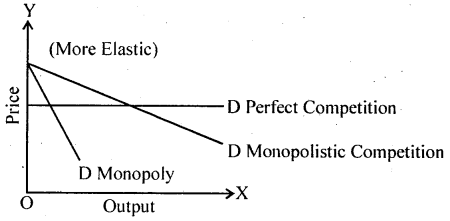

Compare demand curve facing a seller under-conditions of perfect competition: Monopolistic and Monopoly, clearly, reflecting the differences in their elasticities. Draw three curves in a single diagram.

Answer:

Under perfect competition, a firm can sell whole of its output at the same price. Therefore, the demand curve will be a straight line parallel to the X-axis [See fig. (i)].

Under monopoly, a firm can sell more of its product only at a lower price. Therefore, the demand curve of a monopolist is negatively sloped [See fig. (ii)]. Here, demand curve is less elastic.

Under monopolistic competition, a firm can sell more of its product only at a lower price. Therefore, the demand curve of a firm under monopolistic competition is also negatively sloped [Sec fig. (iii)]. Here, demand curve is more elastic.

The difference between the demand curves is that the demand curve under perfect competition is perfectly clastic as the demand curve under monopoly is less elastic than the demand curve under monopolistic competition. This is because of the availability of substitutes in case of monopolistic competition. Close substitutes arc not available in case of monopoly and therefore, demand curve is less elastic under monopoly. The following diagram illustrates the idea:

Question 13.

How is price determined under Monopoly Market?

Answer:

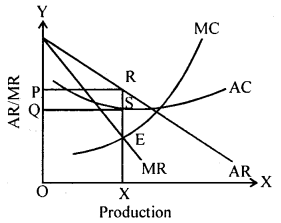

1. Monopoly price or Equilibrium during short period: During short period, monopoly price, normal profit and loss do production work, in three conditions. It is a wrong concept that monopoly always earns profit only during short period. In which situation the monopoly will work under profit, normal profit and loss during short period, it will depend on the demand curve of market and on the cost conditions of the market monopoly firm like the complete competitive finn can also face loss during short period.

In the situation of short period loss, the monopolist will think to do the production upto that point upto which he does not get the cost of the goods equal to Average Variable Cost (AVC) or more than that. Generally monopolist does not get close substitute of the produced goods, because of which the monopolist can make efforts to equal the cost of goods to the average cost in order to prevent his loss during short period but it is only an effort. We cannot deny the possibility of monopoly loss in short period.

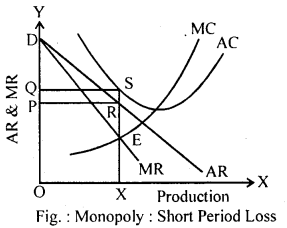

The situation of loss for the monopolist during short period is not the impossible condition. In brief, all the possible situations of monopoly during short period can be understood with the help of following figures:

(i) Profit Situation: The short period profit situation of monopolist is shown in below figure. The demand curve AR of monopoly goods and its related marginal revenue curve MR arc shown in the figure. The balance of monopoly is shown at point E where both the conditions of monopoly balance are being fulfilled. At this point MR = MC. In the situation of this balance, the cost of the goods will be RX or OP. At this cost, the monopolist will do the production of OX goods. In the figure, per unit cost is SX or OQ i.e., the monopolist is getting continuous profit equal to the distance RS. It is clear from the figure that the monopolist will get profit equal to PRSQ on the whole output OX. In brief,

Price = OP

Output = OX

Total Profit = Per Unit Profit × Output

= PQ . OX

= PQRS Area

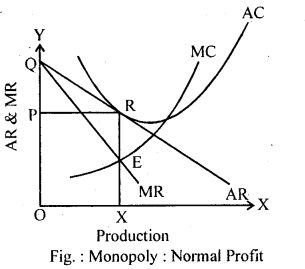

(ii) Situation of Normal Profit: The normal profit of monopolist is shown in adjoining figure. The normal profit is also called zero profit. Normal profit means that the monopolist determines the price of goods equal to the average production cost of the goods. In the figure, the balance point of monopolist is E. Where the average cost of the goods RX and price of the goods both are there. In this situation, the monopolist is not getting any surplus.

Because at point R, AR = AC

In brief, Price = OP

Output = OX

Monopolist is getting zero profit.

(iii) Situation of Loss: The situation of short period loss of monopolist is shown in given figure. The demand of monopoly goods can be so much weak in some circumstances that the price of monopoly goods could be reduced even from the average cost of the goods. It will be the situation of loss. The monopolist on getting more price from the Average Variable Cost (AVC) in short period works in the hope that this loss in the long term will be converted into profit.

In the figure RX is the per unit cost of the goods whereas SX is the average cost of that per unit i.c., per unit output is undergoing loss of SR. The output of goods is OX because of which, the output is under going in loss equal to PRSQ.

In brief, Price = OP

Output = OX

Total Loss = Per unit Loss × Total Output

= QP. OX = PQSR Area

2. Monopoly price or Equilibrium during Long Period: There is complete control of the producer on supply in the monopoly market. Long period is that period of production wherein monopolist fully adjusts his supply according to demand situations. That is why it is said that the price is mainly determined on the basis of supply situations in long period. The monopolist will adjust the supply of the goods in market in order to profit maximisation so that he could get profit in every situation. In short period, the supply could not be adjusted according to demand due to limited period because of which, the conditions of profit, normal profit and loss in short period monopoly market arc created but the monopolist gets only profit due to the adjustment of supply in long period.

The firm and industry get internal and external economics in the beginning due to large scale output in long period but these savings get converted into diseconomies after one point. When the firm and industry get internal and external savings, then the law of increasing returns to scale in applied i.e., the marginal cost gets, decreased gradually on increasing the size of output. As the size of the output gets increases and the marginal cost decreases, then the average cost also decreases but the rate of decreasing of average cost is less than the decreasing of the rate of marginal cost.

In the similar process, we get one such ideal point on increasing more output quantity where marginal cost and average cost should be mutually equal. This, we call the rule of constant returns to scale. After this point, the internal and external savings get converted into diseconomies and the law of decreasing returns to scale is applied! The marginal cost gets increased in such situation. As a result of which, the average cost also gets increased but the marginal cost increases rapidly than the average cost.

All three situations of monopolist in long term increasing returns, constant returns, and decreasing returns get profit.

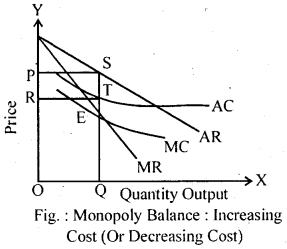

(i) Monopoly Balance in Increasing Returns Situation (or Decreasing cost situation): In following figure the monopoly balance is shown in the increasing returns (or decreasing cost) situation where AC and MC both are declining but MC curve declines more rapidly. According to balance situations, there will be the monopoly balance on point E where both the conditions of balance are being fulfilled.

At balance point E,

Per Unit Price = OP or SQ

Per Unit Cost = OR or TQ

Total Output = OQ

Per Unit Profit = OP – OR = PR or ST

Total Profit PRTS Area.

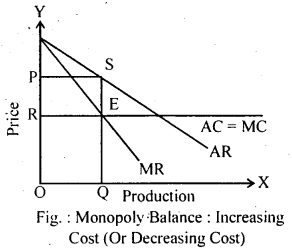

(ii) Monopoly Balance in Constant Returns Situation (or Constant Cost Situation): In following figure the monopoly balance in constant returns situation is shown where average cost and marginal cost are mutually equal due to constant returns.

At balance point E

Per Unit Price = OP or SQ

Per Unit Cost = OR or FQ

Total Output = OQ

Per Unit Profit = PR or SE

Total Profit = PRES Area

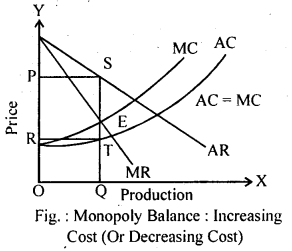

(iii) Monopoly Balance in Decreasing Return Situation (or Increasing Cost Situation): In following figure. Monopoly balance in decreasing returns situation (or increasing cost situation) is shown. Both AC and MC increases due to decreasing returns but MC is more than AC.

At balance point E,

Per Unit Price = OP or SQ

Per Unit Cost = OR or TQ

Total Output = OQ

Per Unit Profit = PR or ST

Total Profit – PRTS Area

Thus, there is profit to monopolist in all kinds of cost situations during long period.

Question 14.

Market for a good is in equilibrium. Explain the chain of reaction in the market if the price is (i) higher than equilibrium price and (ii) lower than equilibrium price.

Answer:

(i) When prices is higher than equilibrium price. There is excess supply and producers are not in a position to sell all they want to sell at the given price.

The leads to competition between producers. Competition between producers leads to lowering of price. Lowering of price raises demand while reduces supply. This continue till demand is equal to supply again at the original equilibrium.

When price is lower than equilibrium price, market demand is greater than market supply. This will result in competition among buyers. The price will rise.

(ii) A rise in price will reduce the demand and raise the supply. This will reduce the original gap between market demand and market supply. These changes will continue till price fiscs to a level at which market demand is equal to market supply. This is the equilibrium price.

Question 15.

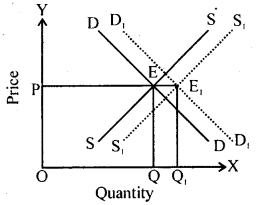

Market for a good is in equilibrium. There is simultaneous ‘increase’ both in demand and supply of the good. Explain its effect on market price.

Answer:

On OX-axis we have plotted quantity and on OY-axis we have plotted price. P is the original price OD is the original demand curve and SS is the

original supply curve and E is the original equilibrium point when demand curve increases from DD to D1D1 and supply curve shifts from SS to S1S1 the new equilibrium point will be formed at E1. Due to which price remains constant and quantity rises from OQ to OQ1.

Question 16.

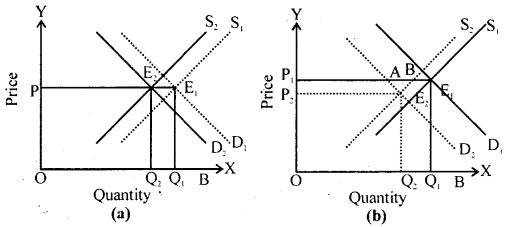

There is a simultaneous ‘decrease’ in demand and supply of a commodity. When will it result in:

(a) NO change in equilibrium price.

(b) A fall in equilibrium price.

Use Diagram.

Answer:

Decrease in demand means less quantity demanded at the same price. This leads to shift to demand curve leftward from D1 to D2 and decrease in supply means less quantity supplied at same price. This leads to leftward shift of supply curve from S1 to S2.

(a) If decrease in demand is equal to decrease in supply there will be no change in equilibrium price. In the diagram (A) the two decrease are equal to Q2Q1. The equilibrium price remains unchanged at OP.

(b) Equilibrium price will fall when decrease in demand is greater that decrease in supply. In diagram (b) decrease in demand (AE1) is greater than decrease in supply (BE1) leading to fall in the equilibrium price from OP1 to OP2.

Question 17.

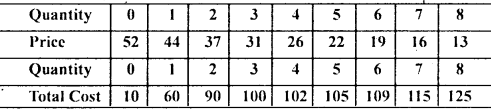

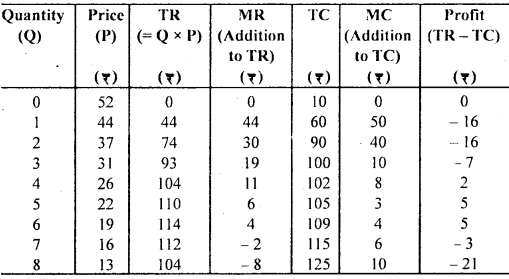

The market demand curve for a commodity and the total cost for a monopoly firm producing the commodity is given by the schedules below, use the information to calculate the following:

(a) The MR and MC schedules.

(b) The quantities for which the MR and MC are equal.

(c) The equilibrium quantity of output and the equilibrium price of the commodity.

(d) The total revenue, total cost and total profit in equilibrium.

Answer:

(a) MR and MC schedules arc given in the table.

(b) At 6th quantity MR and MC are equal.

(c) Equilibrium quantity of output is 6 units and equilibrium price is ₹ 19.

(d) At Equilibrium

TR = ₹ 114

TC = ₹ 109

Profit = ₹ 5

Question 18.

Discuss the method of measurement of National Income?

Answer:

Measurement of National Income: There are three types of Measurement of National Income:

- Product Method or Value Added Method

- Income Method

- Expenditure Method

(1) Value Added Method or Product Method:

First Step: Identification and Classification of Productive Enterprise: At the very first step, we are to identify and classify various productive enterprises of an economy. Broadly speaking, we can classify the economy into the following three sectors:

(i) Primary Sector, (ii) Secondary Sector, (iii) Tertiary Sector. .

(i) Primary Sector: it is that sector which produces goods by exploiting natural resources like land, water, forests, mines, etc. It includes all agricultural and allied activities, such as fishing, forestry, mining and quarrying.

(ii) Secondary Sector: This sector is also known as manufacturing sector. It transforms one type of commodity into another, using men, machines and materials. For example, manufacturing of cloth cotton or sugar from sugarcane.

(iii) Tertiary Sector: This sector is also known as service sector which provides useful services to primary and secondary sectors. It consists of banking, insurance, transport, communication, trade and commerce etc.

Second Step: Calculation of Net Value of Output: To estimate the net value added in each identified enterprise in first step the following estimates arc calculated:

(a) Value of Output, (b) Value of Intermediate Consumption, (c) Consumption of Fixed Capital, i.e., Depreciation.

Value of output is worked out by multiplying the amount of goods and services by each enterprise with their market prices. Value of intermediate consumption is calculated by using the prices paid by the enterprise. Consumption of fixed capital is also estimated as per rules and regulations.

To arrive at the net value added by the enterprise, we have to deduct the following items from the value of output:

- Value of Intermediate Consumption

- Consumption of Fixed Capital

- Net Indirect faxes.

In short,

Value Added = Value of Output – Intermediate Consumption – Net Indirect Taxes

By adding the net value added by all the producing enterprises in an industrial sector, we obtain net value added to that industrial sector. The sum total of net values added by all the industrial sectors in the domestic territory of the country, gives us the Net Domestic Product at Factor Cost.

Hence, Net Value Added = Value Added by Primary Sector + Value Added by Secondary Sector + Value Added by Tertiary Sector.

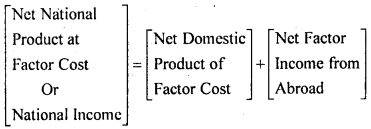

Third Step: Calculation of Net Factor Income from Abroad ;The third and final step in the estimation of national income is to estimate the net factor income earned from abroad and add it to the net domestic product at factor cost. This gives us the national income.

In short,

NNPFC = NDPFC + NFIA

Or

(2) Income Method: In the process of production, different factors like land, labour, capital and organisation co-ordinate with each other and produce goods. These factors belong to household sector and get factor income like rent, wages, interest and profit in return of their services. The sum total of factor’s income is known as national income with income method. This method is also called Factor Payment or Distributed Share Method.

National Income = Wage + Rent + Interest + Dividend + Undistributed Profit + Corporate Profit Tax + Surplus of Public Sector + Mixed Income + Net Income from Abroad.

Where,

Wage: Reward given to labour for his work.

Rent: Reward given to the landlord or owner of building.

It includes imputed rent. Rent of owner occupied houses should be imputed on the basis of prevailing market price and be included in the national income.

Interest: Reward on the capital given as loan.

Profit: Rewards to firms for bearing uncertainties and risks in the production process.

Components of Profit:

- Dividend: A part of the profit which is distributed by the company among shareholders.

- Undistributed Profit: The remaining profit income of the company after paying profit tax and dividend is called the reserve fund which is also known as undistributed profit.

- Corporate Profit Tax: It is a direct tax which government imposes on the profit income of the company.

Mixed Income: Mixed income refers to the incomes of the self-employed persons using their labour, land, capital and entrepreneurship to produce goods and services. These incomes are mixed in terms of wages, rent, interest and profit. That is why it is called mixed income. Such incomes arc also a part of national income.

Surplus of Public Sector: Income earned by public enterprises is also a part of national income.

(3) Expenditure Method:

Expenditure method is the third method for calculating national income under this method, national income is estimated by aggregating all the final expenditure in an economy during a year.

Definition: “Expenditure method is the method which measures the final expenditure on gross domestic product at market price during an accounting year. This total final expenditure is equal to the gross domestic product at market price.”

In expenditure method only final experiditure is taken into consideration. In this method, domestic product is measured as a flow of final expenditure on final goods and services produced in an economy in a year. This final expenditure is termed as ‘Gross Domestic Product at Market Price’ (GDPMP).

Steps in Expenditure Method: Following steps are included in expenditure method in calculating national income:

- Identification of economic units incurring final expenditure.

- Classification of final expenditure.

- Estimation of final expenditure.

- Estimation of net factor income from abroad.

- Estimation of national income.

Step 1. To Identify Economic Units incurring Final Expenditure: Various economic units which incur final expenditure within the domestic territory of a country can be grouped under the following categories:

- Household Sector,

- Producing Sector,

- Government Sector and

- Rest of the World Sector.

Step 2. Classification of Final Expenditure: The final expenditure is classified in the following five main categories:

- Private Final Consumption Expenditure,

- Government Final Consumption Expenditure,

- Gross Fixed Capital Formation (or Gross Fixed Investment Expenditure),

- Change in Stocks (or Inventories),

- Net Exports.

Step 3. Measurement of Final Expenditure on Domestic Product: To get value of gross final expenditure on domestic product, we require two types of data for this purpose:

(a) Volume of Gross Sales, (b) Retail Prices.

By multiplying volume of sales with their respective retail prices and then by adding them all, we get GDPMP.

Step 4. Estimation of Net Factor Income from Abroad: Finally, value of net factor income from abroad (NFIA) is estimated which is added to GDPMP toget GNPMP.

Step 5. Estimation of National Income: For obtaining national income at factor cost, cost of depreciation and net indirect taxes have to be subtracted.

Question 19.

Define budget deficit and trade deficit. The excess of private investment over savings of a country in a particular year was ₹ 2000 crores. The amount of budget deficit was (-) ₹ 1500 crores. What was the volume of trade deficit of that country?

Answer:

Budget deficit means the excess of the government expenditure over tax revenue.

Budget Deficit = Government Expenditure (G) – Tax Revenue (T)

Trade deficit means the excess of import expenditure over the export revenue earned by the economy. Thus,

Trade Deficit = Imports (M) – Exports (X)

Given, G – T = (-)1500

I – S = 2000

Trade Deficit = (I – S) + (G – T)

= 2000 – 1500 = 500 crores

Question 20.

Define production function.

Answer:

A production function expresses the technical relationship between input and output of a firm, It tells us about the maximum quantity of output that can be produced with any given quantities of inputs. If there are two factor inputs, labour (L) and capital (K), then production function can be written as: Q = f(L, K)

where, Q = Quantity of output, L = Units of labour, K = Units of capital.

It may be pointed here that both the inputs are necessary for the production. It any of the inputs is zero, there will be no production with both inputs and output will also be zero. As we increase the amount of any one input, output increases.

Short run is that period of time in which some factor inputs are variable and some are fixed. In this period, a firm can make changes only in the variable factors and not in the fixed factors. On the other hand, a long run is a time period during which a firm can change all factors including machinery, building etc.