BSEB Bihar Board 12th Business Economics Important Questions Short Answer Type Part 3 are the best resource for students which helps in revision.

Bihar Board 12th Business Economics Important Questions Short Answer Type Part 3

Question 1.

Write two examples of Indirect Tax.

Answer:

- Sales Tax

- Entertainment Tax.

Question 2.

Write two demerits of Money.

Answer:

- Money increase corruption

- Money gives rise to inequality of income.

Question 3.

What is Commercial Banks?

Answer:

Commercial Bank is an institution which performs the functions of accepting deposits, granting loans and making investments with the aim of earning profits.

Question 4.

State two features of resources that give rise to an economic problem.

Answer:

Two features of resources that give rise to an economic problem are

- Resources are limited and

- They have alternative uses.

Question 5.

State any two causes of an economic problem.

Answer:

There are two causes of an economic problem:

- Scarcity of resources

- Unlimited human wants.

Question 6.

Write the examples of macroeconomics.

Answer:

The examples of macroeconomics are:

- Aggregate demand

- Aggregate supply

- Employment

- General price level etc.

Question 7.

Write the name of four classical economists.

Answer:

Four classical economists are:

- David Ricardo

- J. B. Say

- J. S. Mill

- Alfred Marshall.

Question 8.

Write two examples of dependent economic variables.

Answer:

- Consumption

- Saving.

Question 9.

Distinguish between micro and macroeconomics.

Answer:

- Microeconomics refers to the analysis of scarcity and choice problems facing a single economic unit such as a producers, a consumer, a firm etc.

- Macroeconomics deals with the supply of economic system as a whole and analysis the behaviour of aggregate such as national income, level of employment and output etc.

Question 10.

What is the difference between monopoly and monopolistic competition?

Answer:

Distinction between Monopoly and Monopolistic Competition:

| Monopoly | Monopolistic Competition |

| 1. Single product and no close substitute. | 1. Product differentiation, i.e., products of firms arc close substitutes. |

| 2. No difference between firm and industry because there is only one firm into the industry. | 2. Group has a large number of firms. |

| 3. AR and MR both fall but AR is relatively less elastic. In pure monopoly condition, demand curve (AR) is rectangular hyperbola which has unit elasticity at all points. | 3. AR and MR both fall but AR is relatively more elastic (but not perfectly elastic like perfect competition). |

| 4. No entry of new firms. | 4. Old firms may quit the group or new firms can join the group. |

Question 11.

What is meant by equilibrium price and equilibrium quantity?

Answer:

Equilibrium Price: The equilibrium price, is the price at which demand and supply are equal to each other or where purchases and sales of buyers and sellers respectively coincide.

Equilibrium Quantity: Equilibrium quantity is that quantity at which quantity demanded is equal to quantity supplied.

Question 12.

What is meant by private income? What is the difference between private income and personal income?

Answer:

Private Income: Private income is the total of factor income from all source and current transfers from the government and rest of the world accruing to private sector.

Difference between private income and personal income:

| Private income | Personal income |

| 1. It is a broader concept than personal income because it includes corporate tax and corporate savings. | 1. It is narrow concept than private income as it does not include corporate tax and corporate savings. |

| 2. It is the total income of both private enterprises and households. | 2. It is the actual income received by households and individuals. |

| 3. Private income = Domestic Income accrued to private sector + NFIA + All Transfer Payments + Interest on National Debts. | 3. Personal income = Private Income – Corporate Tax – Corporate savings. |

Question 13.

Factor income is divided into how many classes?

Answer:

Factor incomes (or factor payments) are broadly classified as under:

- Compensation of employees: The factors payment received by the households for rendering their services as employees of the producing units.

- Rent: The factor payment received by the households for the use of land by the producing units.

- Interest: The factor payment received by the households for the use of their capital by the producing units.

- Profit: The factor payment received by the households for the use of their entrepreneurial skills by the producing units.

Question 14.

What are the precautions related to the calculation of income method?

Answer:

Precautions related to Income Method:

- Income from sale of second hand goods: Any income from the sale of second hand goods and property and it included in national income. But any commission paid on such a transaction becomes the part of national income.

- Transfer payments or incomes: Transfer payments like old age pension, scholarships, unemployment allowance, student’s pocket allowance arc unilateral payments and they are not included in national income.

Question 15.

How national income is calculated by expenditure method?

Answer:

Expenditure method is the method which measures final expenditure on gross domestic product at market price during an accounting year. Final expenditure is equal to the gross domcstric product at market price. This is also called Income Disposal Method or Consumption and Investment Method.

- GDPMP = Private Final Consumption Expenditure + Government Final Consumption Expenditure + Gross Fixed Capital Formation + Net Exports.

- National Income (NNPFC) = GNPMP – Depreciation – Net Indirect Tax + Net Factor Income from abroad.

Question 16.

Explain the relationship between investment multiplier and marginal propensity to consume.

Answer:

Relation between Marginal propensity to consume (MPC) and Multiplier investment: Investment multiplier depends on MPC. Multiplier has positive relation with MPC and negative relation with MPS. Higher the marginal propensity to consume, greater is the size of multiplier. On the contrary, lower the marginal propensity to consume, smaller is the size of multiplier.

Hence, K = \(\frac{1}{1-M P C}=\frac{1}{M P S}\)

When MPC = 0, multiplier will be unity, When MPC = 1, multiplier will be infinity. Hence, the value of multiplier ranges between these two extremes.

Question 17.

Write the names of main measures of monetary polity.

Answer:

Monetary policy: A policy which controls the money supply, credit availability and its cost, is termed as monetary policy. Central bank of the country makes this policy and ensures its execution.

Measures of Monetary Policy:

(A) Quantitative:

- Bank Rate

- Open Market Operations

- Cash Reserve Ratio

- Liquidity Ratio.

(B) Qualitative:

- Moral Pressure

- Margin Requirement of Money

- Credit Rationing.

Question 18.

State any two factors that can cause an increase in demand of a commodity.

Answer:

- Rise in the price of substitute goods.

- Fall in the price of complementary goods.

Question 19.

Explain any two effects of change in income on demand for a good.

Answer:

- Rise in income increases demand for a normal good.

- Fall in income decreases demand for a normal good.

Question 20.

State three causes of increase in supply.

Answer:

The three causes of increase in supply are:

- Rise in number of firms

- Fall in prices of inputs

- Fall in rates of excise duty

Question 21.

Explain the central problem ‘how to produce’.

Answer:

How to produce is the problem of choosing the technique of production. Techniques arc broadly classified into capital intensive and labour intenstive. The problem is to use capital intensive technique in which more of capital goods like machines etc. are used, or to use labour intensive technique in which more of labour is used.

Question 22.

Explain why is production possibility from tier concave?

Answer:

Productive possibility from tier (PPF) is a downward sloping concave curve. Concavity shows increasing marginal rate of transformation (MRT) as more quantity of one good is produced by reducing quantity of the other good. This behaviour of the MRT is based on the assumption that no resource is equally efficient in production of all the goods. As more of one good is produced, less and less efficient resources have to be transferred from the production of the other good which raises marginal cost i.e. MRT.

Question 23.

How does the nature of a commodity influence its price elasticity of demand? Explain.

Answer:

A commodity for a person may be a necessity, a comfort or a luxury.

When a commodity is a necessity its demand is generally inelastic.

When a commodity is a comfort its demand is generally elastic.

When a commodity is a luxury its demand is generally more clastic than the demand for comfort.

Question 24.

What is meant by supply? Mention the salient factors affecting the supply of a commodity.

Answer:

Supply: Supply of goods refers to those qualities which a seller is ready to sell at various price at a certain point of time, like demand supply is also related with a certain time and price.

Factor affecting the supply: Following factors are affecting the supply :

- Price of the commodity: There is a direct relationship between price of a commodity and its quantity supplied. At higher price quantity supplied will be higher and vice-versa.

- Price of related goods: The supply of commodity is also indirectly affected by the price of related goods. For example with increase in price of rice the supply of wheat falls.

- Price of production factors: Supply of a commodity is also affected by the price of production.

- Technology levels: Technology level and its change also affects supply of the commodity. Improvement in the technique of production reduce cost of production and increase supply.

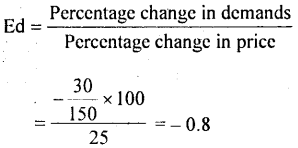

Question 25.

Calculate the price elasticity of demand for a commodity when its price increases by 25% and quantity demanded falls from 150 units to 120 units.

Answer:

Question 26.

Explain ‘what do produce’ with the help of an example.

Answer:

‘What to produce’ is a problem which deals with what type of commodity we have to produce, (i.e. either consumer goods or capital goods) and in what quantity. If we are producing consumer goods, then we have to sacrifice the production of capital goods.

Question 27.

Distinguish between ordinal and cardinal analysis.

Answer:

- Ordinal analysis is a form of analysis in which utility is compared in terms of ranks not in the terms of number.

- Cardinal analysis is a form of analysis in which utility is measured in terms of number not in ranks.

Question 28.

State any three causes of leftward shift of demand curve.

Answer:

- A rise in price of a complementary good.

- Fall in income of consumer.

- Unfavourable changes in consumer taste and preferences.

Question 29.

Why rise in price leads to fall in demand?

Answer:

- Income effect: It refers to changes in quantity demanded when real income or buyer change due to change price of the commodity.

- Substitution effect: It refers to substitution of one commodity for the other when it becomes relatively cheaper.

- Size of consumer groups: When price of a commodity falls, it attracts new buyers who now can afford to buy it.

Question 30.

Explain product homogeneity feature of perfect competition.

Answer:

Product homogeneity is one of the basic feature of perfect competition. Homogeneous products are identical in quality, shape, size, colour, design, packing etc. This implies that the products sold by different firms in the market are equal and have no distinction for the buyers. They are not only standardised products but arc also perfect substitutes of each other and their cross elasticity is infinite. Since a buyer can not differentiate between the product of one firm, and that of another, he becomes indifferent as to the firm from-which he buys. For him sellers are same. The product being homogeneous and identical, as a result no seller can charge a price higher than the given market price.

Question 31.

Explain free entry and exit of firms’ feature of perfect, competition.

Answer:

Entry into the market and exit from the market is free under perfect competition. This means that new firm is free to start production if it wishes and that any existing firm is free to lease production and leave the industry if it wishes so. The existence of free entry wid free exist will ensure that the firm earns only normal profits in the long run.

Question 32.

Distinguish between change in quantity demanded and change in demand.

Answer:

Difference between change in quantity demanded and change in demand are follows are:

| Change in quantity demanded | Change in demand |

| 1. When quantity demanded changes due to change in price of the commodity but other thing remaining constant. | 1. When demand changes due to change in other factors but price of the commodity remains constant. |

| 2. Extention and contraction are the part of change in quantity demanded. | 2. Increase and decrease in demand are the part of change in demand. |

| 3. It is due to the rise or fall in price. | 3. It is due to the following, reasons: (i) Change in price of substitute goods. (ii) Change in income of consumer (iii) Change in consumer taste and preference. |

Question 33.

Explain the implication of large number of buyers and large number of sellers in case of perfect competition.

Answer:

There are large number of buyers and sellers in case of perfect competition because nobody can influence the prices of a commodity, neither the individual buyer nor the individual seller.

Question 34.

How can be control the prices of a commodity?

Answer:

We can control the prices of a commodity in the following ways:

- By reducing the consumption of the commodity.

- By using the substitute of the commodity.

- By importing the commodity from some other country.

Question 35.

Explain any two causes of decrease in supply of a commodity.

Answer:

Two causes of decrease in supply are:

1. Case of outdated technology: When we use outdated technology that results in decrease in supply. It is the period of 21st century, we have to use new technology but when we use outdated technology instead of new one, that affects in supply of a commodity.

2. Increase in price of factors of production causing increase in production may lead to increase in cost which may decreases the profit margin, due to which supply decreases.

Question 36.

Distinguish between product differentiation and price discrimination.

Answer:

Product differentiation means when product is same but it is differentiated on the basis of packaging, labelling, handling etc. It exists in case of monopoly.

Price diescrimination means when same product is sold to different customers at different prices. It exists in case of monopolistic competition.

Question 37.

Total revenue at a price of Rs. 4 per unit of a commodity is Rs. 480. Total revenue increases by Rs. 240 when its price rises by 25 percent. Calculate its price elasticity of supply.

Answer:

| P (RS.) |

TR (Rs.) |

Supply (uts) |

| 4

5 |

480

720 |

120

144 |

ΔS = 144 – 120 = 24

ΔP = 5 – 4 = 1

ES = \(\frac{\Delta \mathrm{S}}{\Delta \mathrm{P}} \times \frac{P}{\mathrm{~S}}=\frac{24}{1} \times \frac{4}{120}=0.8\)

ES < 1

It is unitary elastic.

Question 38.

State any three main features of monopolistic competition.

Answer:

The three main features of monopolistic competition are:

- There are large number of buyers and sellers.

- There is freedom of entry and exist of firms.

- Product differentiation.

Question 39.

How can demand of alcoholic drinks and arms can be reduced?

Answer:

Demand of alcoholic drinks can be reduced by imposing more of taxes on them because increases in taxes leads to decrease in demand of a commodity and decrease in demand of alcoholic drinks will help society also.

Question 40.

The price elasticity of demand for a good is (-1). 50 units of goods are bought at a price of Rs. 4 per unit. How many units of it will be bought at a price of Rs. 6 per unit?

Answer:

Ed = \(\frac{\Delta Q}{\Delta P} \times \frac{P}{Q}\)

(-1) = \(\frac{\Delta Q}{2} \times \frac{4}{50}\)

ΔQ = 25

Since, there is an inverse relation between price and quantity, as a result of increase in price the quantity demanded will decrease by 50 – 25 = 25 units.

Question 41.

What does a production possibility curve shows? When will it shift to the right?

Answer:

A production possibility curve shows the different combination of goods that can be produced with the given limited resources and technology.

The production possibility curve shifts towards its right, if there is an increase in the supply of resources due to technological progress. For examples better equipments, superior methods or techniques of production. When such technological changes take place there the economy can produce more goods. This results in a shift of the production possibility curve.

Question 42.

Explain why a production possibility curve is concave?

Answer:

A production possibility curve is concave due to increasing marginal rate of transformation (MRT) as more quantity of one good is produced by reducing more and more quantity of the other good. This behaviour of the MRT is based on the assumption that all resources are not equally efficient in production of all goods. As a result of it, marginal rate of transformation increases.

Question 43.

State three features of monopoly.

Answer:

The three main features of monopoly are as follows

- There is only one seller or producer of a commodity in the market.

- A monopolist can change different prices for his product from different persons and in different market areas.

- The monopolist controls the situation in a such a way so that it becomes very difficult for a new firm to enter the monopoly market and complete with the monopolist by producing a homogeneous or identical product.

Question 44.

Explain the problem of ‘for whom to produce’.

Answer:

The problem ‘for whom to produce’ is related to the question at a given level of various goods and services, who gets how much to consume. This implies that who earns how much or who has more assets than other. For example, how much a doctor consume is based on his earnings compared to a clerk. The purchasing power depends mainly on the distribution of national income among the factors of production.

Question 45.

Why do problem related to allocation of resources in an economy arise?

Answer:

Every economy has to face economic problems relating to allocation of resources. Following are the main factors that lead to economic problems:

- Wants are unlimited having different uses: All human wants are unlimited and recurring. All human wants are not important.

- Means are limited with alternative uses: Our resources are limited. This gives rise to economic problem. The problem becomes more worse because the unlimited means have alternative uses.

- Adjustment between means and wants: The economic problem, arises because adjustments have to be made between limited means with alternative uses and unlimited wants.

Question 46.

Explain the causes of a leftward shift in demand curve of a commodity.

Answer:

Causes of leftward shift of demand curve:

1. A fall in income of the consumers: As the income of the consumers falls, the demand for normal goods normally falls at a given price and as a result, the demand curve of the commodity shifts to the left. It implies decrease in demand.

2. A fall in the price of substitute goods: When the price of substitute goods (say coffee) falls, the demand curve of the commodity shifts to the left. It implies decrease in demand.

3. A rise in the price of complementary goods-when the price of complementary goods (say petrol) rises. not only its demand falls but the demand for its related goods (say car) also falls and as a result; the demand curve of the commodity shift to the left. It implies decrease in demand.

Question 47.

Explain the difference between an inferior good and a normal good.

Answer:

Difference between an inferior good and a normal good are follows:

| Normal good | Inferior good |

| 1. When rise in income leads to rise in demand for a good, that good is called normal good. | 1. When rise in income leads to fall in demand for a good, that good is called an inferior good. |

| 2. There is a direct (positive) relationship between income and demand for a normal good. | 2. There is an inverse (negative) relationship between income and demand for an inferior good. |